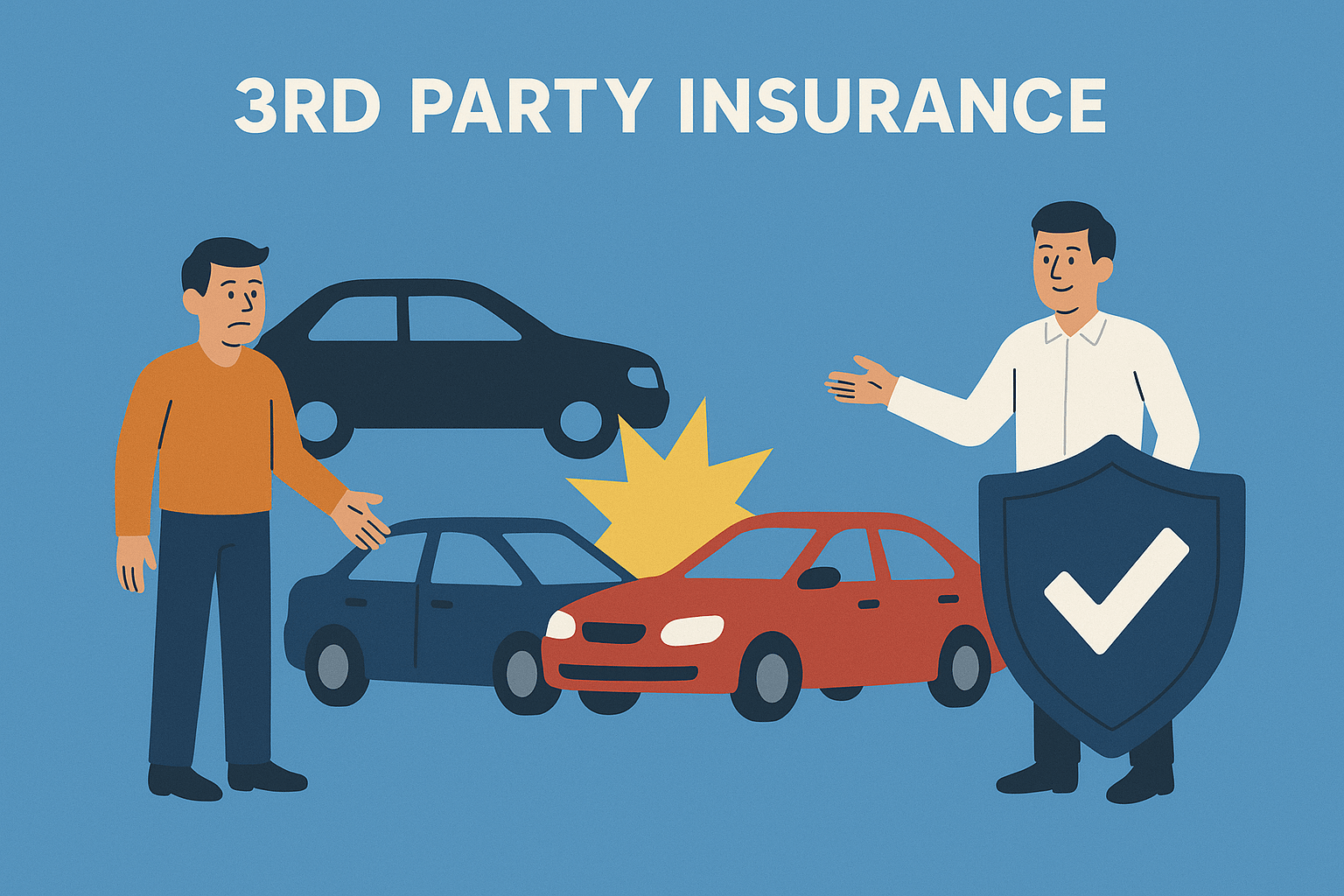

What You Need to Know About Driving on Third Party Insurance in Kenya (2025 Guide)

What You Need to Know About Driving on Third Party Insurance in Kenya (2025 Guide)

If you're a Kenyan driver trying to keep your insurance costs low, chances are you've considered—or already purchased—third party insurance. It’s the most basic motor insurance cover in Kenya and is legally required for all vehicles on the road. But what does it actually cover, where does it fall short, and when might it actually be the best option for you?

Let’s break it down.

✅ What Is Third Party Insurance?

Third party insurance covers only damages or injuries caused to other people (the “third party”) in an accident where you're at fault. In Kenya, this is the minimum legal requirement for all motorists under the Motor Vehicle Insurance (Third Party Risks) Act (Cap 405).

It typically covers:

- Injuries to other people (pedestrians, passengers, or drivers in other vehicles)

- Damage to other vehicles or property

- Legal fees if you're sued for the accident

But—and this is important—it does NOT cover:

- Damage to your own vehicle

- Theft of your car

- Fire damage

- Personal injury to you, the driver

🏆 Benefits of Third Party Insurance in Kenya

1. Affordability

Third party premiums in Kenya are among the lowest. For many car owners—especially matatus, boda bodas, and small private car operators—this makes it a go-to option. Prices can start as low as KES 5,000–7,500 annually, depending on the insurer and vehicle type.

2. Legal Compliance

It helps you avoid fines and penalties. Driving without valid insurance in Kenya is a serious offence that could result in a KES 50,000 fine, a jail term of up to 1 year, or both under Kenyan traffic laws.

3. Simple Claims Process for Third Parties

If you injure someone or damage property, the process of compensating them is relatively straightforward through your insurer.

⚠️ Pitfalls and Vulnerabilities of Third Party Insurance

1. No Protection for Your Car

If you hit a pothole and damage your suspension, your third party policy won't help. If your car is stolen or catches fire? You're on your own.

2. No Cover for Your Own Medical Bills

In case of injury, you’ll pay for your own hospital bills unless you have a separate personal accident or medical cover.

3. Limited Theft Protection

In carjack-prone areas or if you regularly park in unsecured places, you’re particularly vulnerable. Third party insurance offers no financial safety net for car theft.

4. Doesn't Cover Natural Disasters

Think floods in Nairobi’s South C, or falling trees in Karen during storms. If Mother Nature strikes, your insurer doesn’t pay a cent under third party.

🧠 When Third Party Insurance May Actually Be the Smarter Option

Despite the drawbacks, there are scenarios where third party makes more financial and practical sense:

✅ You're Driving an Old or Low-Value Vehicle

If the cost of a comprehensive cover is more than 10% of your car’s value, third party might be better. It’s not worth paying high premiums for a car that’s already depreciated heavily.

✅ You Rarely Drive

If your vehicle spends more time parked than driven (e.g., a secondary car or a car in the village), it may not justify the cost of full coverage.

✅ You're Only Using It Short-Term

If you're between jobs or saving for a better car, third party can be a temporary, budget-friendly choice.

🔐 How to Address Third Party Insurance Weaknesses

The good news? You can plug the coverage gaps with smart add-ons or alternative policies:

1. Personal Accident Cover (PAC)

This is one of the best add-ons you can buy. For just KES 1,000–5,000 per year, you can get coverage of up to KES 500,000–1,000,000 for injuries, disability, or death—for you and your passengers.

📌 Top providers offering good PACs in Kenya include: APA, Jubilee, CIC, Britam, and AAR.

2. Standalone Theft Protection

Some insurers allow limited theft/fire add-ons on top of a third party cover. This gives you partial peace of mind for carjackings or fire damage.

3. Medical Insurance

A NHIF cover or a private inpatient/outpatient cover ensures you're not footing hospital bills alone. Especially important if you're using public roads regularly.

4. Trackers and Anti-theft Devices

If you drive in high-theft areas, installing a tracker or immobilizer can reduce theft risk—and some insurers may even give discounts on add-ons if you have these installed.

📝 Final Thoughts: Is Third Party Insurance Right for You?

Third party insurance in Kenya isn’t for everyone. But if you’re strategic—say, driving a low-value vehicle, using the car sparingly, or combining it with smart add-ons—it can be the most economical legal option. Just be honest about your exposure and supplement it with the right safety nets.

If you're unsure, ask your insurance provider whether you can upgrade to a hybrid package or negotiate an affordable enhanced third-party cover.

📢 BONUS TIP: How to Check If Your Insurance is Valid

You can easily verify your motor insurance via https://www.ira.go.ke or by using the NTSA app for added security.

Remember!

If you need quick, transparent logbook loan, contact us through our contact form, call us on +254791573231 or visit one of our branches across Nairobi, Kiambu, Machakos, and Kajiado counties to explore your financial options.

Comments ()